GMX: cash flow is king

GMX has been in the top 5 protocols by fees generated recently, surpassing stalwarts such as Bitcoin, Curve, AAVE and Compound. What makes the protocol tick? Find out in this deep dive.

What is GMX?

GMX is a decentralized spot and perpetuals exchange on Arbitrum and Avalanche, allowing users to take up to 30x leverage on trading perpetuals. According to the protocol’s own documentation, it aims to support trading with low swap fees and zero impact trades. GMX facilitates this through a multi-asset pool, called the GLP pool, which lets liquidity providers earn fees through market making, swap fees and leverage trading being done on the platform.

Analyzing GMX from a product and market perspective:

A majority of trading of crypto assets and derivatives even today happens largely on centralized exchanges like Binance, Coinbase and FTX. This is mainly because they are usually the point of entry for a new user (enabling the fiat to crypto on-ramp) and provide intuitive and responsive UX, which usually results in users sticking to the same platform and not shifting to a decentralized, on-chain alternative. However, increasing on-chain activity, token launches and the rise of the DeFi ecosystem in general, along with increasing regulatory concerns on centralized exchanges (for example, Binance eliminating leverage trading in Europe) make a strong case for trading activity to significantly increase on-chain, due to the permissionless nature of on-chain trading protocols.

This indeed has been the case, with DEX spot volume % rising over the past year.

Source: The Block

The success of Uniswap, however, has spawned many copy-cat projects. Perpetual trading protocols are still nascent. This leaves a gap in the market for an on-chain protocol which supports both spot and perpetuals (as most centralized exchanges like FTX/Binance do) which is profitable for token holders as well.

GMX aims to fill and capitalize on this gap in the market, and with trading activity continuously increasing on-chain, and is well positioned to become the ‘on-chain FTX or Binance’. With a unique token incentive structure and a sophisticated set of features, it also means that GMX is difficult to copy or ‘fork’, which is not the case with simple spot DEXes as mentioned above. This gives GMX an edge in the market. However, like the centralized exchange ecosystem, there is a good chance that there might be a similar oligopoly, with Gains Network being the major up and coming competitor, with others like Mycelium and MUX also trying to come in, and incumbents like dYdX making radical moves (migrating to its own Cosmos chain)

GMX protocol and token mechanics:

Although the competition in the decentralized spot/perpetual markets is growing, GMX has managed to carve out a special place for itself amidst the rising competition through its novel protocol mechanics and tokenomics.

For starters, its GLP liquidity pool model enables traders to perform zero-slippage trades, as opposed to Uniswap’s AMM model where traders have to incur some slippage on swaps.

GMX also prevents the phenomenon of scamwicks, one of the most detrimental features in which happens when individuals or institutions trade at a price far out of the current trading range, which causes users’ stop losses to be triggered, initiating a domino effect of buy/sells which causes the price to move in the direction in which they want it to move.

A typical scam wick:

Source: TradingView

In order to avoid this, GMX uses the GLP pool along with dynamic price feeds provided by Chainlink, which in turn pull and verify price data from FTX and Binance, which allows the protocol to determine the true price of an asset and enable users to trade with zero slippage.

The GLP liquidity pool to swap assets and go long/short on them is one of the major innovations on the platform. It consists of various assets (ETH, BTC, UNI, LINK, stablecoins etc.) which the liquidity providers can deposit to the pool, and in exchange mint GLP tokens on the same. Since the pool does not utilize the traditional AMM model, LPs providing liquidity to the pool don’t have to worry about impermanent loss as well.

There is a fee incurred on minting GLP tokens. This fee goes lower the higher the demand for that particular asset in the pool is.

For example, in the above instance, since the supply of ETH in the pool is low and demand is the highest, the fees for minting GLP by depositing ETH is the lowest.

You can also burn GLP tokens to redeem any of the assets in the pool, according to the dollar-denominated value of both GLP and the asset to be redeemed (1:1) - minus some fees.

Unlike traditional margin trading however, where users borrow assets to go short and stablecoins to go long, users on GMX borrow assets to go long and stablecoins to go short. This essentially means that GLP holders are renting out their spot exposure to traders.

This means that if traders on GMX make a profit, GLP holders make a loss, and vice-versa. Historical statistics suggest that on an average, traders have always made a loss.

Source: GMX stats

GMX is the protocol’s governance and utility token, used to vote on governance and the future roadmap of the protocol. Staking GMX also unlocks benefits, which we will see in the next section.

Revenue generation and token value accrual:

The protocol generates revenue through charging fees on opening and closing positions and a borrow fee which is deducted every hour a leveraged position is open.

This revenue is entirely distributed to GMX and GLP holders, with 70% of the fees going to GLP holders and 30% to staked GMX holders. Since the protocol is deployed on both Arbitrum and Avalanche, GLP holders get 70% of the protocol fees in AVAX on Avalanche and in ETH on Ethereum. Similar denomination is followed for staked GMX depending on the network on which it is staked.

The GMX tokens accrues value mainly through it being staked, which is most likely the reason why roughly 84% of the total circulating supply has been staked.

Staked GMX earns rewards (and hence accrues value) through three ways:

Escrowed GMX (esGMX): this token can be staked for rewards similar to normal GMX, or vested to become normal GMX tokens over a period of one year.

Current Distribution of esGMX:

100,000 esGMX tokens per month to GMX stakers

100,000 esGMX tokens per month to GLP holders on Arbitrum

50,000 esGMX tokens per month to GLP holders on Avalanche from Jan 2022 - Mar 2022

25,000 esGMX tokens per month to GLP holders on Avalanche from Apr 2022 - Dec 2022

2. Multiplier points: basically an incentive mechanism to reward long-term holders by increasing rewards at a constant rate every second GMX is staked, which comes out to be 100% APR, meaning that x amount of GMX staked over one year will accrue the same rewards as if 2x amount of GMX was staked.

3. ETH/AVAX rewards: rewards denominated in ETH/AVAX (depending on network where GMX is staked) coming from the protocol revenue.

GMX also has a floor price fund which guarantees a lower bound on its price. accumulates capital through fees on the protocol owned GMX/ETH liquidity and 50% of the funds in Olympus bonds, can be used to buyback and burn GMX if

Current floor price fund: $2,977,696

Total supply of GMX: 13,250,000

Hence, minimum price of GMX (floor price) guaranteed by the fund is:

$(2,977,696/13,250,000) = $0.224

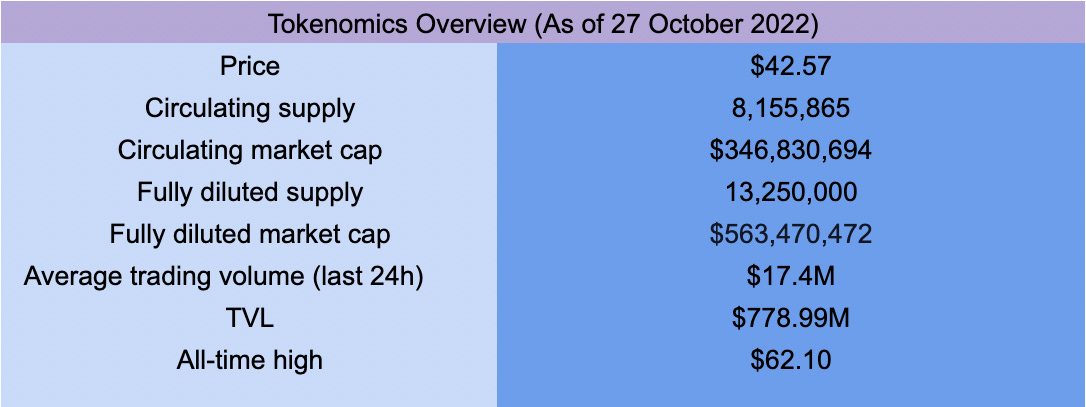

Tokenomics:

A broad overview of the tokenomics of the protocol is as follows:

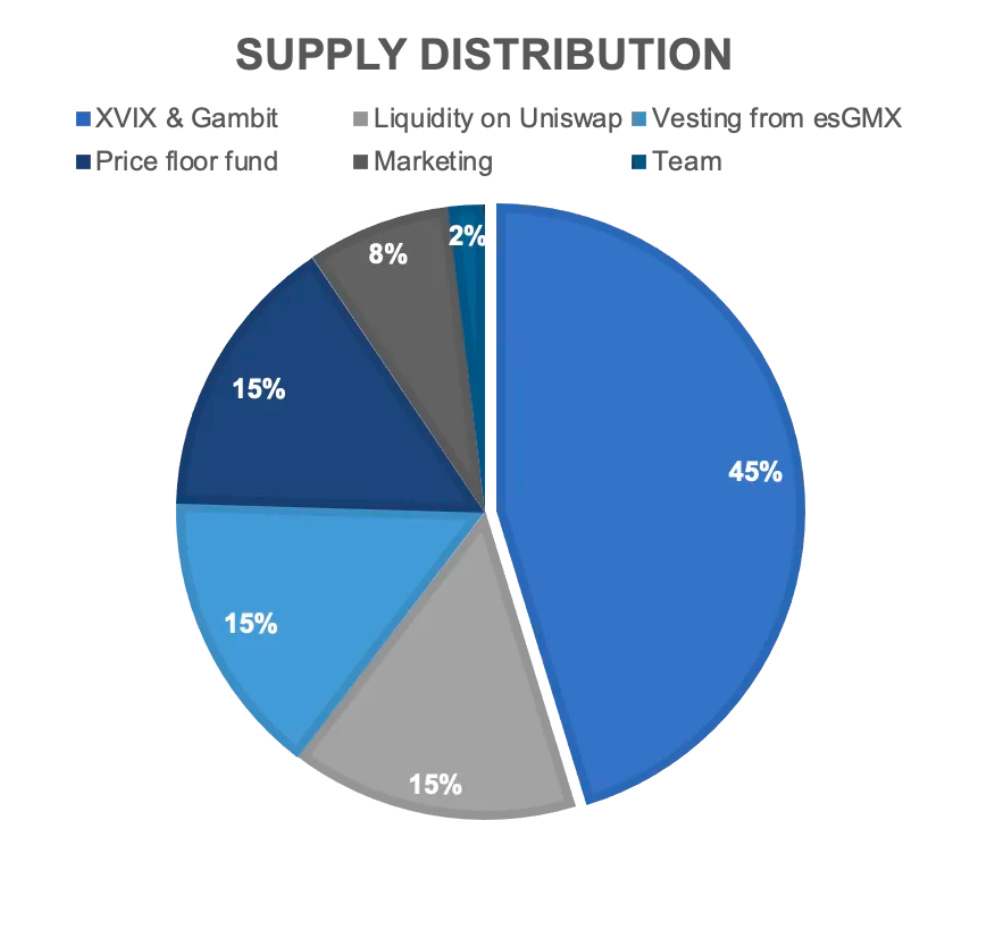

Even though the total supply is 13.25 million, of these, 2 million are reserved for emissions arising out of staking esGMX, which may not even be completed, making GMX extremely scarce.

The detailed token distribution is given below:

GMX was initially launched as Gambit Financial on the Binance Smart Chain (BSC) but later rebranded to GMX when it launched on Arbitrum, and has had zero fundraising.

The fundraise for Gambit and XVIX were public community raises and both of these projects had their tokens and liquidity migrated to GMX. VCs and notable investors have therefore had to buy from the public market.

Conclusion:

GMX is well-positioned to be one of the top players in the decentralized perpetuals market. However, with competitors like Gains Network, Mycelium and MUX coming in, it will be interesting to see who gets to dominate the market in the long run. But seeing GMX in the top 5 protocols by fees generated, makes one thing perfectly clear: cash flow is king.

Disclaimer: AGBuild (AlphaGrep Securities) may hold positions in one or more of the tokens mentioned in this article. None of this is financial advice.